How to manage your finance effectively?

In the book of “Rich dad Poor dad” by R.Kiyosaki and S.Lechter, it is stated that we usually earn a living thanks to our skills, and most of students graduating from colleges are not equipped any financial skills, resulting in facing several financial issues even though they are successful with their career.

This blog therefore took inspiration from invaluable lessons written in that book and other books on the financial topics, together with the writer’s experience, and then shared three simple yet effective tips for you, as whoever you are, to self-manage your finance.

#1: Create a Personal Balance Sheet and Personal Income Statement in an Excel worksheet

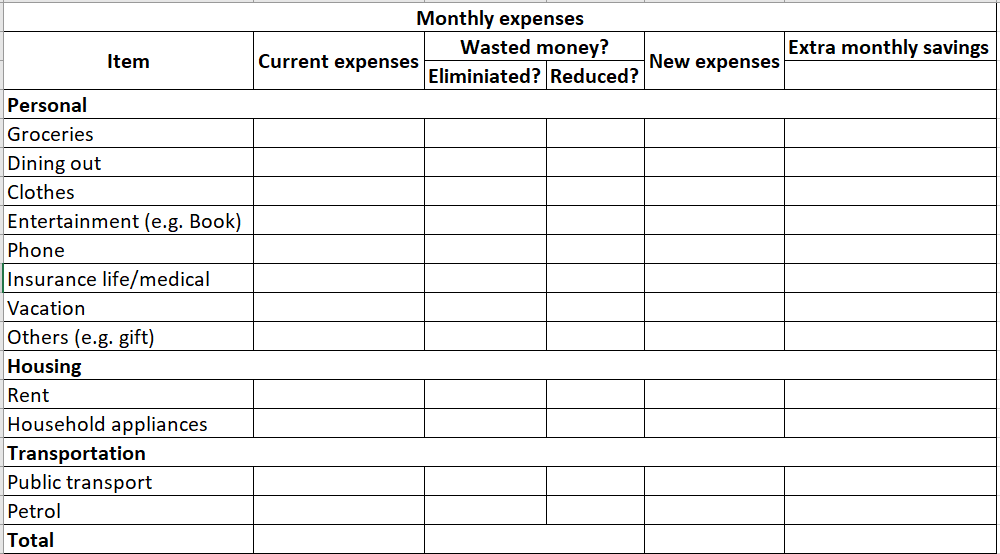

The personal balance sheet simply tells you the inflow and outflow of your money, so it is actually helpful to answer the question that you might have monthly “Where are all my money gone?”. You should update this table every month. After a year, you can fill in your Personal Income Statement. Looking at this table shows you which part accounts for most of your income/outcome.

It is not difficult to do, but there are some tricks you should remember:

• Your transaction comes from several sources (e.g. bank account, cash, credit card, etc.), so ensure to note down them in your Personal Balance Sheet regularly. A good way is to keep your bill/receipt/invoice.

• A mantra is “Always SPEND < EARN”. This means your expenses should be smaller than your income, or your liabilities should always be less than your assets.

#2: Study the two tables

An interesting fact that I learned for myself is that you can save money yourself by around 20-25% monthly if you read the figures of your Personal Balance Sheet and Income Statement. You will be surprised to realize that lots of your purchases were unnecessary. For example, I could have brought my water along when biking, instead of getting a 2-euro cola at the supermarket. These things does not sound like a matter, but it actually happens more often than you think. Therefore, an effective way is to create a daily expense table besides the aforementioned tables. You fill in details of everything you bought and consider which can be reduced or eliminated. After all, you got a new expense, which is supposed to be lower than your current expenses. Subtracting them to see how much you can have more monthly if you do not waste your money on those.

#3: Read more books, especially on financial topics

The great Soviet writer Maxim Gorky once said “Love books, a source of knowledge”. That is how I have learned to manage my finance effectively. With respect to financial topics, there are usually two kind of books such as self-help and technical. The first one is aiming at providing mental techniques on how to think as a millionaire, while the second one concentrates mainly on illustrating knowledge and technical things (e.g. how to read a graph, how to find a good stock, etc.). Sometimes there are also a combined kind of books. One of the most similar points of those books is not to work for money, but because of your passion. Similarly, in the book of “What I wish I knew when I was 20”, T.Seelig suggested that success comes when your passion, skills, and market needs meet each other. At the end of this section, you can find a list of financial books that you may be interested in.

• Rich dad poor dad (R.Kiyosaki & S.Lechter, 1997)

• The new Buffettology (D.Clark, 2002)

• Common stocks and Uncommon stocks (Philip Fisher, 1996)

• Grinding it out: The Making of McDonald (R.Kroc & R.Anderson. 1977)

• Awaken the Giant Within (A.Robbins, 1991)

• The winning investment habits of Warren Buffett & George Soros (M.Tier, 2004)

Please don’t hesitate to share this very useful information for those needing insights on personal finance!

Series Excel skills

-

Work Smart – How to automate repetitive emails?

Example of a VBA macro that automates sending repetitive Outlook emails.

-

Upgrade your Excel skills: A smarter way of visualizing your data in Excel

Visualizing data in Excel by creating charts and graphs.

-

Analyze data in Excel with a case study of Dry Port to Dry Port (Part 2)

Data analysis in Excel with a case study of Dry Port to Dry Port (Part 2)

-

Analyze data in Excel with a case study of Dry Port to Dry Port (Part 1)

Practical example on how to collect, clean and analyse data in Excel.

-

How to manage your finance effectively?

How to manage your finance effectively and how to create a Personal Balance Sheet and Personal Income Statement in an Excel worksheet.

Share this

0 Comments